01 · The street lender

A small loan kept growing.

In Thailand and the Philippines, people we know faced the same pattern: borrow a little, owe much more the next week, then owe more again when the first due date becomes impossible.

Our story

Moodeng began with a simple refusal: a small loan should never grow without warning, expose someone’s private life, or turn a hard week into public shame.

Where it started

The worst credit products do not look complicated. They start with a small amount, then use a growing price, pressure, and shame to make it impossible to leave.

01 · The street lender

In Thailand and the Philippines, people we know faced the same pattern: borrow a little, owe much more the next week, then owe more again when the first due date becomes impossible.

02 · The app version

Some loan apps replaced the collector at the door with access to contacts, family, coworkers, and public messages. The interface looked cleaner, but the fear was the same.

03 · A different rail

USDC and Base made it possible to move small amounts through a global digital-dollar network without building the experience around bank transfer overhead. That created room for a person-to-person model with no Moodeng service fee.

04 · Moodeng

A borrower chooses the reason, expected payback, and date. A person chooses whether to fund it. The outcome stays on a record the borrower can build, without giving Moodeng access to a private phone.

The rules we keep

These are not campaign promises. They shape what Moodeng asks for, what funders see, and how the team responds when repayment is difficult.

The humans

Moodeng is early. The people shaping the product are still close to the borrowers, lenders, and support questions that show where it needs to improve.

Judge the product, not the story

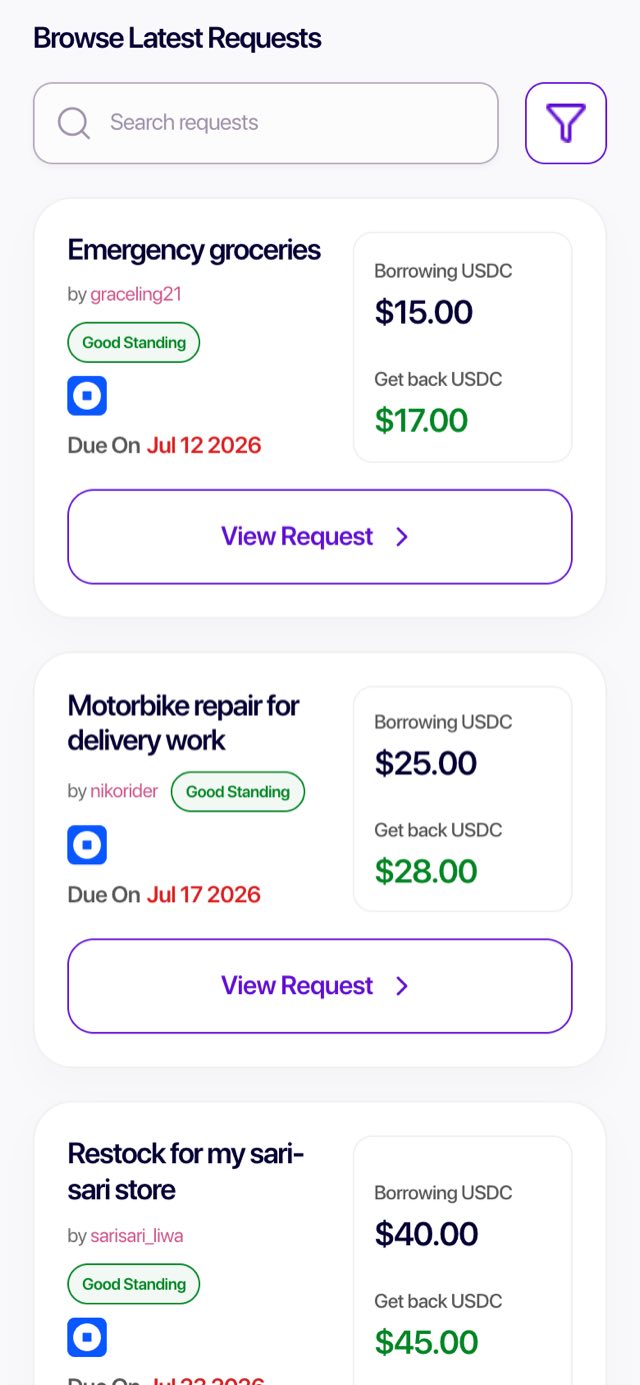

The product tour and request board are open before you create an account.